Managing money can feel overwhelming, especially when you are trying to balance bills, savings, and everyday spending. The 50/30/20 budget rule offers a simple way to organize your finances without getting lost in details. It breaks your income into three clear categories, making it easier to see where your money goes. For many people in the United States, the 50/30/20 method can serve as a starting point for building better financial habits and gaining more control over spending.

Understanding the 50/30/20 Rule

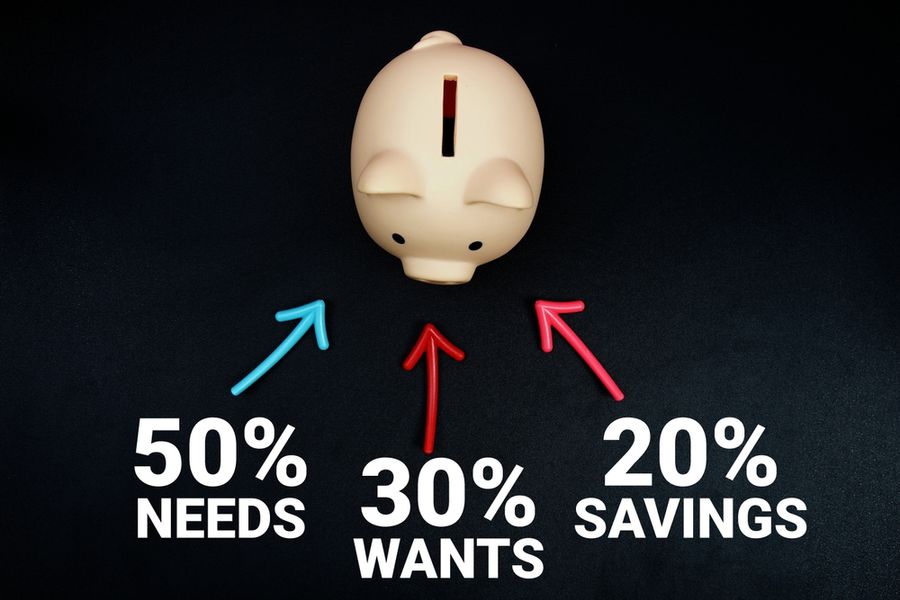

The 50/30/20 rule divides your after-tax income into three parts: needs, wants, and savings. The idea is that about half of your income goes toward essential expenses, a portion goes toward personal spending, and the rest is set aside for saving or paying down debt.

“Needs” include things you must pay to live and work, such as housing, utilities, groceries, and basic transportation. “Wants” cover non-essential spending like dining out, entertainment, or shopping. The final portion is for savings, which can include building an emergency fund, contributing to retirement accounts, or paying off existing debt.

This structure is meant to be flexible. It gives you a clear framework without requiring you to track every single purchase in detail.

How to Apply the Rule to Your Income

To get started, first calculate your monthly income after taxes. This is the amount you actually have available to spend. Once you know that number, you can begin dividing it into the three categories.

Start by listing your fixed expenses, such as rent or mortgage payments and utilities. These will usually fall under the “needs” category. Then review your variable spending, like groceries and transportation, and include those as well. After that, identify your “wants,” which may include subscriptions, dining out, or hobbies.

The remaining portion of your income should be directed toward savings or debt repayment. If your current spending does not match the 50/30/20 split, that is okay. The goal is to gradually move closer to this balance over time.

Adjusting the Rule for Real Life

While the 50/30/20 rule is simple, real-life expenses do not always fit neatly into fixed percentages. In some areas of the United States, housing costs alone may take up more than half of your income. In these cases, it is important to adapt the rule rather than abandon it.

You can treat the percentages as guidelines instead of strict limits. For example, if your “needs” category is higher, you may need to reduce spending in the “wants” category or find ways to increase your income. The key is to stay aware of your overall balance and make choices that support your financial goals.

Flexibility is what makes this method useful. It helps you understand your priorities without forcing you into an unrealistic structure.

Common Mistakes to Avoid

One common mistake is misclassifying expenses. It can be easy to label non-essential spending as a “need,” which can throw off your budget. Being honest about what is truly necessary helps keep your plan accurate.

Another issue is ignoring savings. Some people focus so much on covering expenses that they forget to set aside money for the future. Even small contributions to savings can make a difference over time, so it is important to include this category from the start.

It is also important to avoid making too many changes at once. Trying to completely overhaul your spending habits overnight can be difficult to maintain. Instead, focus on gradual improvements that you can stick with over time.

Building Consistency With the 50/30/20 Approach

Consistency is key when using the 50/30/20 rule. Rather than aiming for perfection, focus on building habits that support your budget. This might include checking your spending regularly or setting up automatic transfers to your savings account.

Over time, these small actions can help you stay on track without requiring constant effort. The goal is to create a system that works in the background, allowing you to manage your money with less stress.

It can also help to review your budget at the end of each month. This gives you a chance to see what worked, what did not, and where you can make adjustments. Regular reviews keep your plan aligned with your current needs and goals.

Turning a Simple Rule Into a Lasting Habit

The 50/30/20 budget rule offers a clear and flexible way to manage your money without overcomplicating the process. By dividing your income into needs, wants, and savings, you can build a better understanding of your spending habits and make more informed decisions.

While the percentages may need to be adjusted to fit your situation, the core idea remains useful. With consistency and small changes over time, this approach can support long-term financial stability and confidence.